17 / 90

17 / 90

14

F I G . 1 :

FOUR FUTURE SCENAR I OS FOR THE D I AMOND I NDUSTRY

1

DIAMONDS

ARE FOREVER

Consumer demand grows strongly, fuelled by recovery in the US economy and continued above-

average growth in emerging markets, especially China and India. Brands become more important and

increasingly invest in promoting the allure of diamonds. Even with demand in Europe and Japan

softening, the dynamics of supply and demand in this scenario mean that previously uneconomical

mining projects become economically viable, so production is maximised.

2

DEMAND

SHOCK

Diamond demand grows more slowly as key consumer markets such as the US, China and India

experience weak growth. Companies lose the incentive to invest heavily in brands, and diamonds lose

some appeal through a lack of investment in promoting the diamond category and consumers moving

away from conspicuous consumption. Production remains stagnant but recycling of diamond jewellery

increases as consumers encounter financial distress.

3

FEAST AND

FAMINE

The diamond industry develops in a volatile manner, driven by high levels of global macro-economic

uncertainty. Strong rises in demand are followed by sharp decreases, leading to scattered supply

expansion. Lead-time between the demand and supply cycles implies a wide variation in prices.

Mining companies strive to diversify their mining assets to manage volatility and adapt to the growing

resource nationalism trend. Consumers increasingly move away from diamonds, and brands slow down

their investments.

4

EAST RENEWS

GLOBAL

GROWTH

The industry enjoys strong growth driven by emerging markets, especially China and India. However,

US growth is only moderate. The consumer base for diamonds widens as the emerging middle class

grows and consumers show a distinct preference for brands. Diamond producers will continue to invest

in developing new supply projects.

McKinsey recently published a report,

'Perspectives on the Diamond Industry'.

Building on four key uncertainties, the macro-

economic outlook, future consolidation in the value chain, consumer attitudes to diamonds, and the supply of rough

diamonds, the report identified four future scenarios for the global diamond industry.

Source: McKinsey & Company,

‘Perspectives on the Diamond Industry’,

September 2014

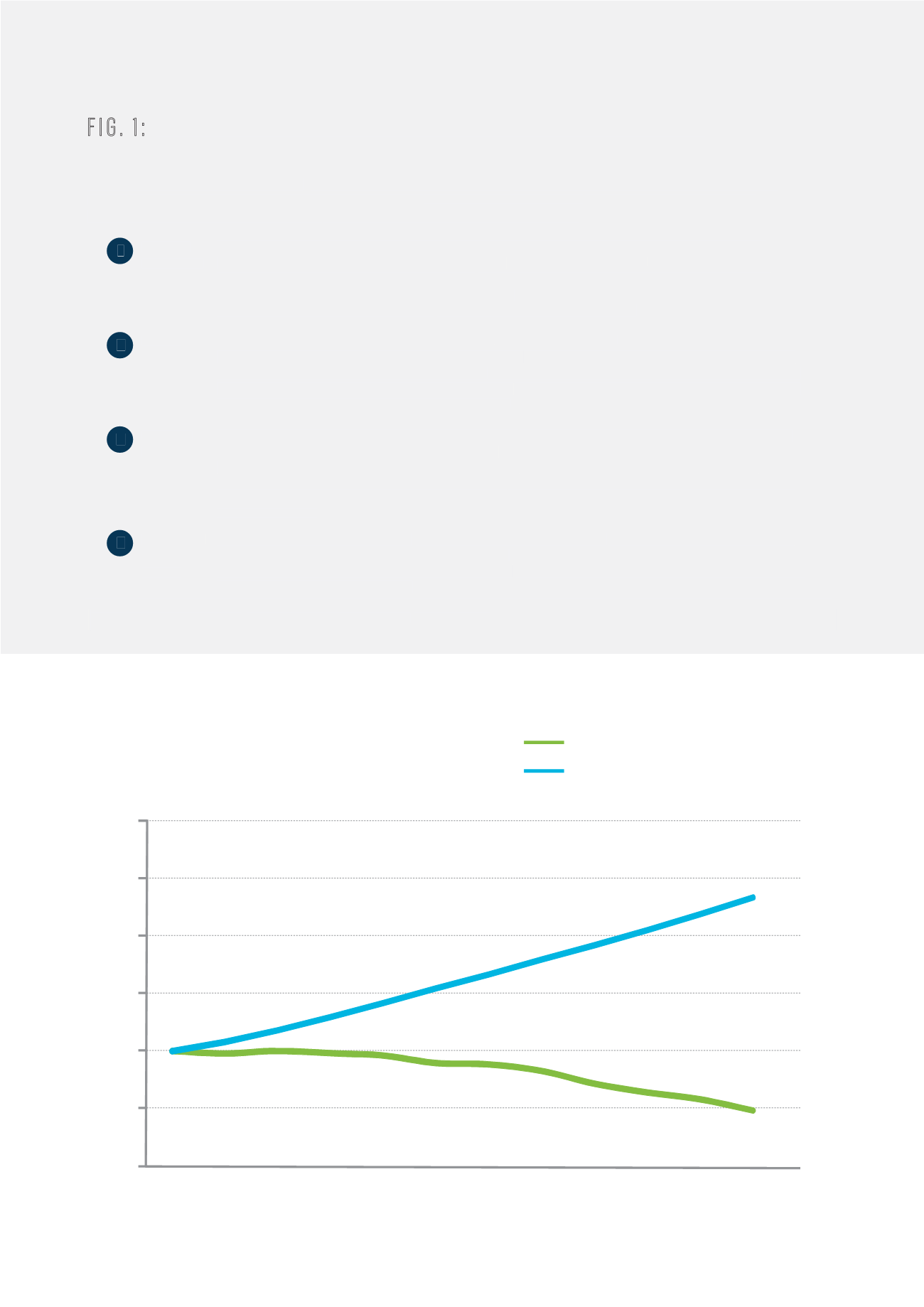

Source: De Beers analysis, McKinsey & Company,

‘Perspectives on the Diamond Industry’,

September 2014

F I G . 2 :

SUPPLY AND DEMAND CURVE BASED ON ‘ D I AMONDS ARE FOREVER ’

SCENAR I O

Demand forecast value in nominal terms (smoothed)

Production forecast in value at 2013 prices

2025F

2024F

2023F

2022F

2021F

2020F

2019F

2018F

2017F

2016F

2015F

2014F

60

80

100

120

140

160

180

Index base 100 in 2014