19 / 90

19 / 90

16

Source: De Beers

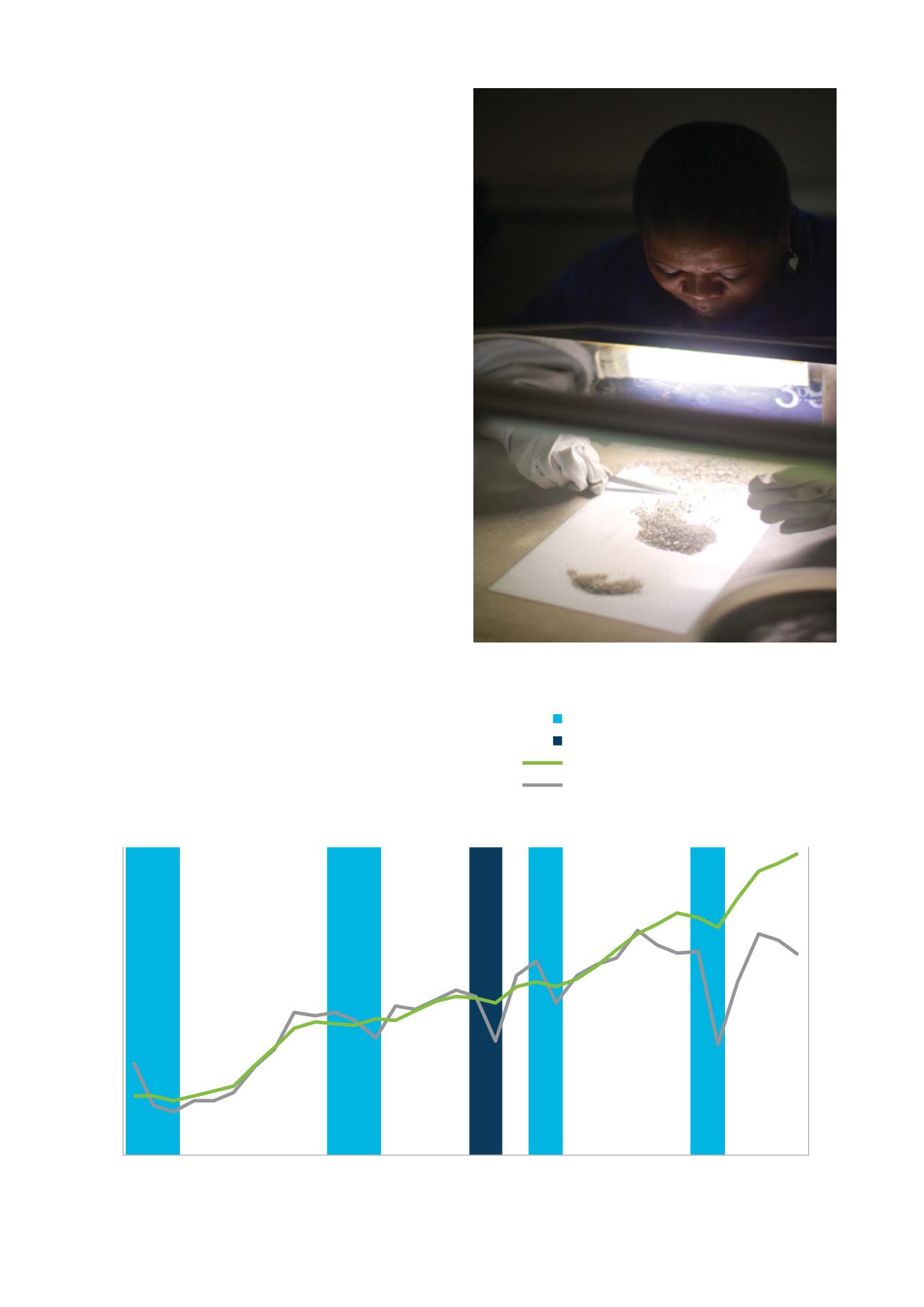

F I G . 4 :

CONSUMER DEMAND AND DE BEERS ROUGH D I AMOND SALES

OVER T IME ( 1 980 - 20 1 3 )

Nominal De Beers rough diamond sales

US recession years

Asia/Japan financial crisis

Consumer demand (Nominal USD PWP)

20

15

10

5

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1987

1986

1985

1984

1988

1982

1981

1980

1983

0

3

6

USD billion

0

25

9

NOMINAL

DEBEERS

ROUGH SALES

PWP

However, the positive supply demand outlook can be

expected to be impacted by the cyclical nature of the

industry. It is especially prone to the ‘ripple effect’

caused by de-stocking and re-stocking by midstream

operators to fulfil lower or higher demand. Despite

this, over the past 50 years rough diamond values have

consistently recovered as economic growth rebounds

(see Fig. 4).

THERE ARE TWO KEY ASPECTS TO THE HEALTH OF THE

DIAMOND INDUSTRY IN THE NEAR FUTURE

The first is

safeguarding and nurturing the diamond

dream

– that is, the allure that diamonds have for

consumers, based on their association with romance

and a sense of the eternal, and the fact that they are

seen as a lasting source of value. As always, changing

consumer preferences, competition from other

luxury categories, and – among other risks – the

potential confusion caused by undisclosed synthetics

and treatments all pose challenges for the entire

diamond industry.

The second is

innovation and differentiation

to take

full advantage of opportunities created by the expected

growth in diamond demand.